Nearly half of Veterans (49%) feel homeownership is currently out of reach, according to a recent survey from NewDay USA.

But many are closer than they think. And you might be, too.

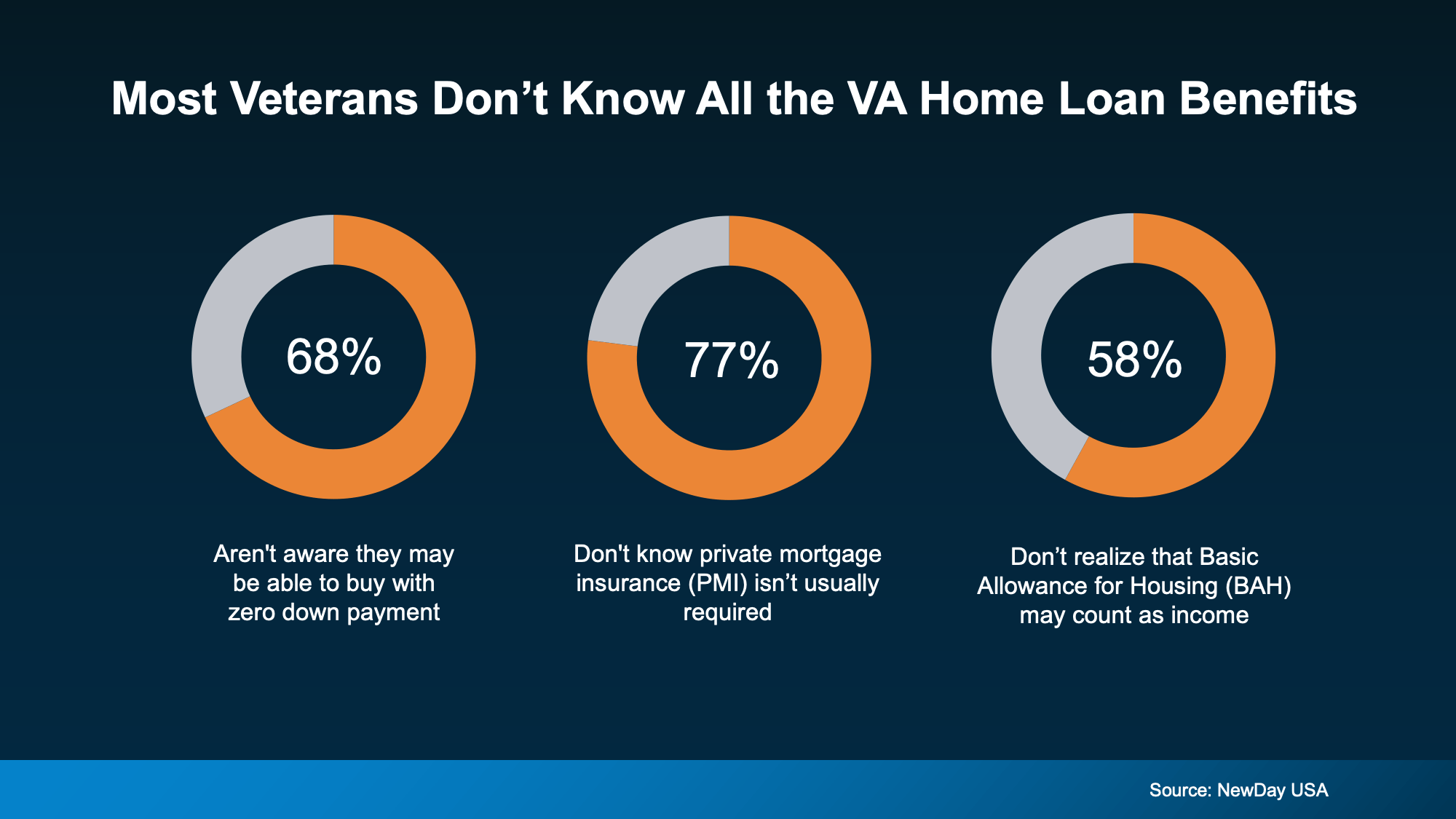

If you’re a Veteran, you probably know the Veterans Affairs (VA) home loan benefit exists – it's been around for over 80 years. What you might not know is what it actually covers. Three misconceptions trip up Veterans the most (see graph below):

Any one of those beliefs could be holding you back. Let’s walk through all three, so you have the information you really need.

Any one of those beliefs could be holding you back. Let’s walk through all three, so you have the information you really need.

You May Not Have To Put Any Money Down

The potential to put zero money down is probably the biggest perk of a VA loan, but most homebuyers don’t even realize that’s an option. According to the NewDay USA survey, many respondents guessed they’d need to save somewhere between $10,000 and $19,900 before they could buy. That’s years of saving for an upfront cost that isn’t always required.

You May Have Lower Closing Costs

According to the Department of Veterans Affairs, with VA loans, there can be limits on the types of closing costs buyers have to pay. That means more money stays in your pocket on closing day – and you have less to save up for before you can buy. The benefit combined with the down payment perk can speed up your buying timeline.

Your Monthly PMI Costs Could Be $0

Unlike many other loan options, VA loans typically don’t require private mortgage insurance (PMI), even with low or no money down. If you take out a conventional loan instead, you could pay $100 to $300 a month in PMI until you hit 20% equity, according to NewDay USA. Over time, that’s a difference of thousands of dollars.

Your BAH & BAS May Help You Qualify for More

If you’re on active duty or if you’re a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan. So, if you were running the numbers without factoring your BAH or BAS in, you could qualify for more than you thought. Both BAH and BAS are non-taxable, so they can help raise the amount you can qualify for.

Bottom Line

VA home loans can put homeownership within reach, and a trusted lender can help make sure you understand the details before you move forward.

If you’re active duty, you’ve served, or know someone who has, connect with a trusted lender who can walk you through whether you’d qualify and what the VA benefit offers. You may be able to buy a home sooner than you thought.

Check out this article next

Leave a Reply